The Baltics are doing alright when it comes to defence tech growth, according to a newly published report.

Iron Wolf Capital, Startup Estonia, Startup Lithuania, and WALLESS have published the third annual Baltic Deep Tech Report 2025.

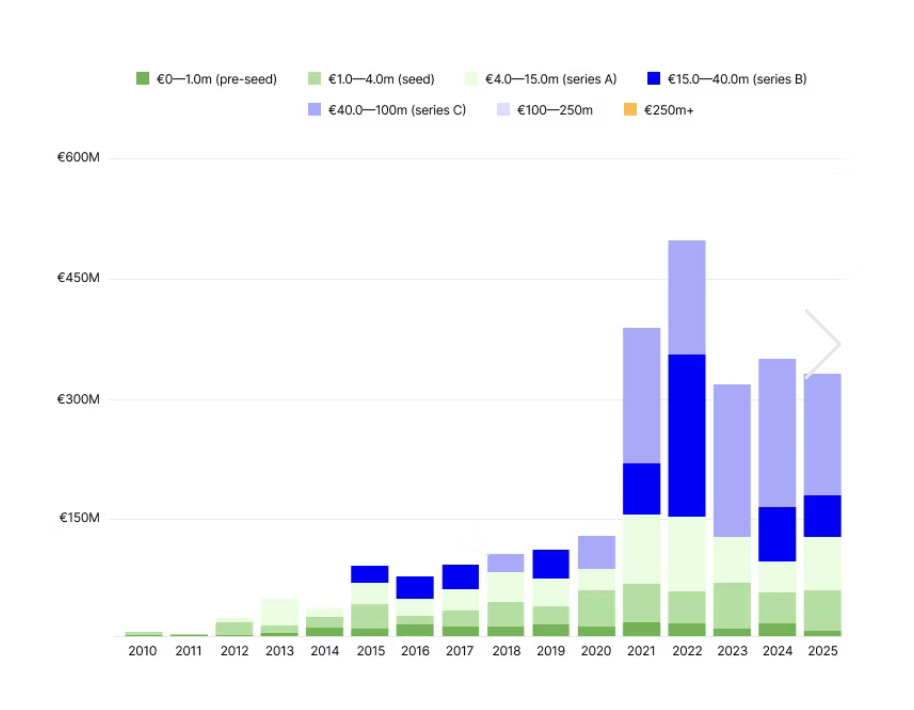

Overall, some €328 million across 106 funding rounds was invested in deep tech in the Baltics in the year, up 160% on 2020’s investments of €126 million. As a sector, deep tech is huge in the Baltics, accounting for more than 49% of all tech investments in the period.

Early stage investments continue to dominate: 20.5% of all investments were Series A, up 79% on 2024, and more than half of investments at Series B and blow, and nothing later than Series C in series or size, as the graph below shows.

But perhaps one of the biggest takeaways is that startups, investors, and the technology sector overall are all responding forcefully to world events — not least world events unfolding in their backyard.

Specifically, DSR — the overall category covering defence, security, and resilience — stands out in the report as one of the defining technology sectors of 2025 in the Baltics.

The data-driven deep dive into the region’s deep tech startup economy finds that “defence technology has emerged as its fastest-accelerating dimension.”

This directly reflects not just the war in Ukraine but also the resulting unease over what Russia will do next along the Eastern Flank: the bottom line is that Europe is hustling now to get up to speed in its defences, and the Baltics are arguably (and literally) on the front line of that activity.

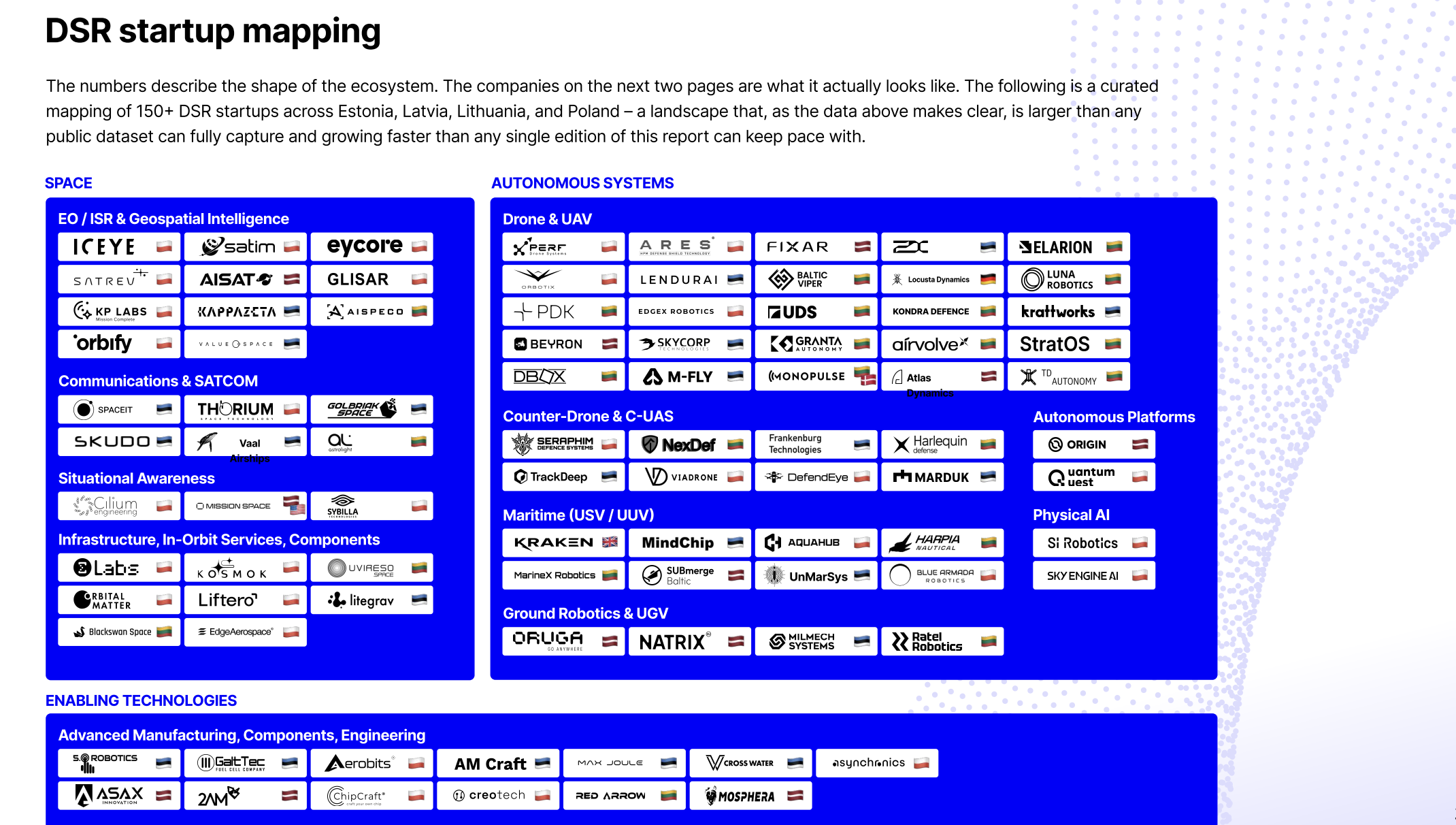

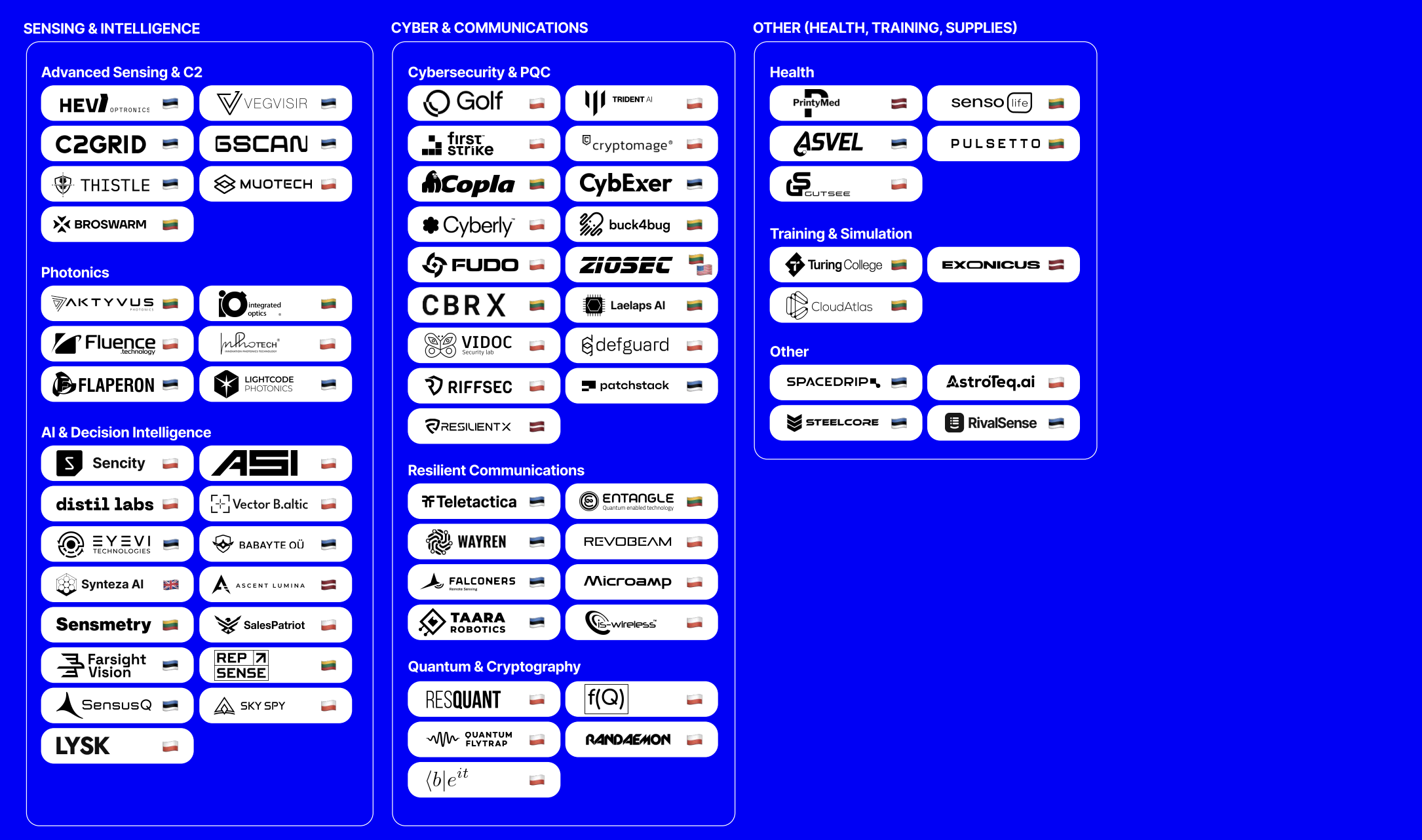

After mapping 150+ DSR startups and a total of €104 million in announced funding across 47 rounds, the highest growing verticals are energy, robotics, and autonomous systems.

The data is based on publicly-announced deals, meaning it does not include what is being built — and funded — in stealth, which is not uncommon in the DSR sector.

Iron Wolf detailed 47 publicly-announced funding rounds in the DSR sector, which accounted for 15.4% of all startup funding in the Baltics in 2025.

Within that year, the largest rounds went to firewall firm Blackwall (€45 million), hydrogen fuel cells scale-up PowerUp Technologies (€10 million), navigation startup Lendurai €5.5m million, comms platform Wayren ($7.9 million), superbattery scaleup Skeleton Technologies ($7 million) and short range missile systems startup Frankenburg Technologies ($4 million).

Since 2025, some of these startups have gone on to raise more: for example, Frankenburg confirmed a further €30 million in funding in February. And we are hearing murmurs of a several other fundraisings in the works right now, so it seems we are far from peak fundraising in DSR in Europe.

Some of the activity is disproportionate to the scale of the nations themselves, another signal of how much geopolitics are driving startup activity (and investor interest).

For example, Estonia ranks 7th in Europe for VC funding in the defence sector, ahead of countries with ten times its population of 1.4 million, the report notes. The authors do not break out a hard number for money raised but notes that Estonia was the highest-ranking Baltic country for overall tech investment at €353 million.

Others have some room for growth on that front: Lithuania and Latvia are respectively 16th and 21st on the list for DSR investments. And Poland, despite having the sixth-largest economy in the EU and the eighth-largest in Europe overall, may well be disproportionately behind on startup activity and funding.

Although Poland committed 4.7% of its $1.1 trillion in GDP to defence in 2025 — the highest proportion of any NATO country — it noted that just €19.4 million in disclosed funding was raised across 18 early-stage rounds into startups in the sector. Investor share is approximately 61% domestic investment.

You can find the full report here.